Please sign in or register

Existing users sign in here

Having trouble signing in?

Contact Customer Support at

[email protected]

or call+852 3175 1913

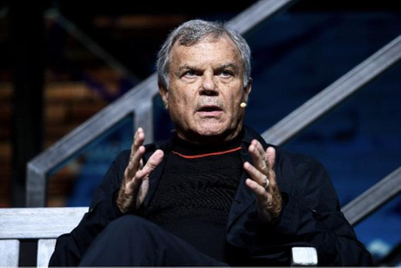

WPP’s chief executive gives his take on the global economy, the shift to digital, short-termism, and the prospect of Google buying agencies.

Contact Customer Support at

[email protected]

or call+852 3175 1913

Top news, insights and analysis every weekday

Sign up for Campaign Bulletins

Ogilvy APAC celebrated a strong creative year in 2024, clinching top regional honours at Cannes Lions. Yet operational headwinds, particularly in China, tested its resilience and reshaped its growth strategy.

Ogilvy and UM win global network of the year awards for creative and media respectively, while Special agency in New Zealand earns Asia-Pacific network of the year.

.png&h=268&w=401&q=100&v=20250320&c=1)

Apple’s new Japan campaign tells the real-life story of a heavy metal fan whose Apple Watch alerts help detect a life-threatening heart condition just in time.

A ubiquitous surname, a sexually transmitted infection, the printing of memories and an animal god that helps gamers might all bring fame glory to campaigns in Cannes next week.

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.png&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=268&w=401&q=100&v=20250320&c=1)

.png&h=268&w=401&q=100&v=20250320&c=1)