According to ZO’s April 2014 global ad forecast, Asia’s more ‘advanced markets’ (Australia, New Zealand, Hong Kong, Singapore and South Korea) will make up in 2014 for a year of disappointing 2 per cent growth in 2013, rising to 4.9 per cent. This will be followed by 6.7 per cent growth in 2015 and 5 per cent in 2016.

The agency categorises the rest of Asia as ‘fast-track’ thanks to the speed at which these developing economies are growing. According to ZO, fast-track Asia barely noticed the 2009 downturn (ad expenditure grew by 7.3 per cent that year) and since then has recorded strong growth. Ad expenditure in Fast-track Asia grew 11.0 per cent in 2013, and the agency forecasts growth of between 11 per cent and 13 per cent a year for 2014 to 2016.

Japan, as in many reports, is an outlier in Asia and gets handled separately. Despite recent measures of economic stimulus, Japan remains stuck in its rut of persistent low growth, according to the report. Japan grew 2.0 per cent in 2013, and ZenithOptimedia expects the growth rate to remain at 2 per cent a year through to 2016.

ZO also expects the world’s fastest-growing markets to supplant many of the countries currently on the top-10 leaderboard. In 2013 France ranked eighth among the world’s markets and Canada ranked ninth. By 2016 ZO expects France to have fallen to 10th and Canada to 11th. Canada will be pushed out of the top 10 by Indonesia, which is forecast to rise from 13th to eighth over the same period. Meanwhile South Korea will rise from 10th to ninth.

Mobile advertising spend

ZO estimates global expenditure on mobile advertising to be $13.4 billion last year, representing 12.9 per cent of internet expenditure and 2.7 per cent of total advertising expenditure. By 2016, the agency forecasts, this total will rise to $45 billion, which will be 28 per cent of internet expenditure and 7.6 per cent of all expenditure. This means mobile will leapfrog radio, magazines and outdoor to become the world’s fourth-largest medium by the end of the forecast period.

“Mobile advertising (by which we mean all internet ads delivered to smartphones and tablets, whether display, classified or search, and including in-app ads) has now truly taken off and is growing six times faster than desktop internet,” said ZO. “We forecast mobile advertising to grow by an average of 50 per cent a year between 2013 and 2016, driven by the rapid adoption of smartphones and tablets. By contrast we forecast desktop internet advertising to grow at an average of 8 per cent a year.”

ZO’s findings are slightly more optimistic than an earlier report by Gartner, but nevertheless tally fairly closely overall. According to Gartner, mobile ad spend is expected to reach $18 billion in 2014 and will reach $42 billion by 2017.

"Over the next few years, growth in [global] mobile advertising spending will slow due to ad space inventory supply growing faster than demand, as the number of mobile websites and applications increases faster than brands request ad space on mobile device screens," said Stephanie Baghdassarian, research director at Gartner. "However, from 2015 to 2017, growth will be fuelled by improved market conditions, such as provider consolidation, measurement standardization and new targeting technologies, along with a sustained interest in the mobile medium from advertisers."

Asia-Pacific and Japan, which have been driving global mobile advertising growth till now are expected to slow down in the years ahead and North America is forecast to rise and take the lead. “In Asia/Pacific and Japan the maturity of mobile advertising is inducing a slowdown in revenue growth,” said Gartner. Nonetheless, Asia’s mobile advertising from 2012 through 2017 is expected to average 30 per cent per year.

"North America is the region with the strongest general advertising focus and investment. It is also the region where online advertising is most mature," said Mike McGuire, research vice-president at Gartner. "Overall advertising budgets are the highest, so when a portion shifts to mobile, in a multiplatform approach, it immediately impacts the market's scale."

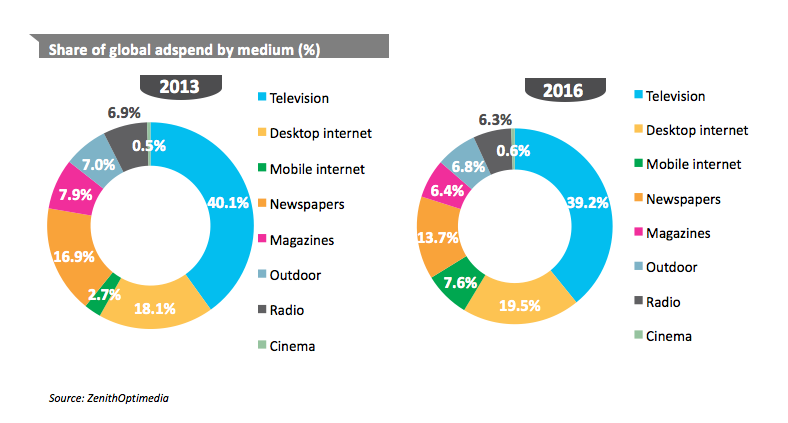

Global advertising spend by medium

According to ZO, online is still the fastest growing medium globally. It grew 16.2 per cent in 2013, and the agency forecasts an average of 16 per cent annual growth for 2014 to 2016. In this category, display is the fastest growing sub-category with 21 per cent annual growth thanks to the rise of social media advertising, which is growing at 29 per cent a year. Online video is also starting to be sold by programmatic buying, providing advertisers with more control and better value. ZO expects online video to grow at 23 per cent a year for the rest of the forecast period.

"Globally, television is still the top advertising medium, attracting 40 per cent of spend in 2013," ZO said. "Despite this, television’s share of global adspend is likely to fall back slightly over the next few years as desktop and mobile internet grow much faster. Television’s market share has grown steadily over the last three and a half decades, from 30.7 per cent of spend in 1980 to 40.1 per cent in 2013. We think it has now peaked, however, and forecast it to fall back marginally to 39.2 per cent in 2016."

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=334&w=500&q=100&v=20250320&c=1)

.png&h=334&w=500&q=100&v=20250320&c=1)

.png&h=334&w=500&q=100&v=20250320&c=1)

.jpg&h=268&w=401&q=100&v=20250320&c=1)

.jpg&h=268&w=401&q=100&v=20250320&c=1)

.png&h=268&w=401&q=100&v=20250320&c=1)